These are some common concerns investors have expressed over the past few months. We’ll explore these concerns in a 5-part email series covering key areas such as market timing, diversification, managing risk, managing market emotions and the benefits of regular investing.

Understanding the value of dollar cost averaging can help clients stay calm and stay invested

Your clients may be nervous about investing during volatile markets, but this is when dollar cost averaging really shines. Dips in the market allow clients to buy more units when prices are low and fewer units when prices are high, which over time may help to smooth out the effects of market fluctuations.

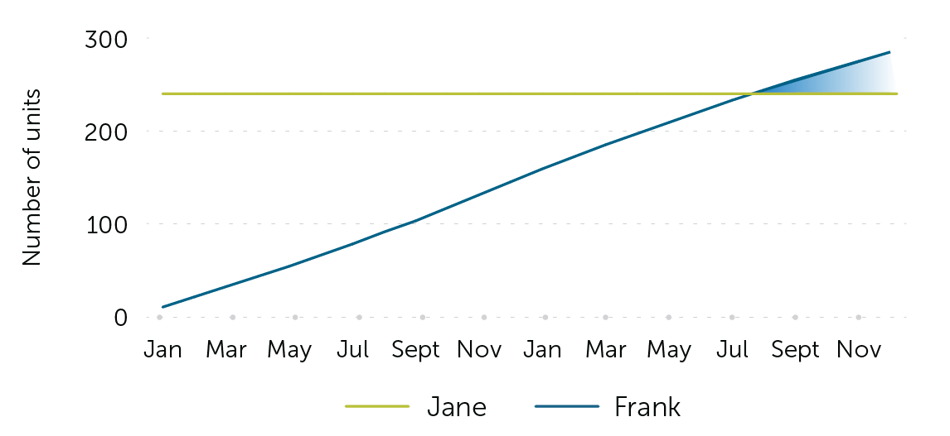

Let’s compare two investors: Jane and Frank both invest $2,400 in the same fund.*

Dollar cost averaging

*The market values quoted are hypothetical and for illustrative purposes only. They should not be considered representative of past or future investment performance.

Jane, shown by the green line on the graph, made a lump-sum investment, purchasing 240 units at $10 per unit. The number of units she owns remains the same throughout the time period. Frank made monthly contributions of $100 for 24 months. Because he bought some units in a market dip, Frank's average unit price was $8.41 and he purchased 285 units. The number of units he owns increases with each monthly contribution, as shown by the blue line. With dollar cost averaging, Frank was able to capitalize on periods of market dips to acquire more units at the end of the period than Jane.

Share this investor friendly flyer with your clients to show them an example of how dollar cost averaging works and how it can benefit them by;

Bringing discipline to an investment plan

Helping to avoid timing the markets

Purchasing more units when prices are low.

Today’s challenging and volatile markets are an ideal time to discuss the benefits of dollar cost averaging with your clients.

These award-winning funds exemplify the Investment team’s disciplined investment style, with a strong emphasis on finding attractively valued, high quality businesses, with a focus on downside protection.

1 Policies issued by The Empire Life Insurance Company.

Stay tuned for next week’s email about ways to manage risk.

Segregated Fund contracts are issued by The Empire Life Insurance Company (“Empire Life”). A description of the key features of the individual variable insurance contract is contained in the Information Folder for the product being considered. Any amount that is allocated to a segregated fund is invested at the risk of the contract owner and may increase or decrease in value. Please read the information folder, contract and fund facts before investing. Past performance is no guarantee of future performance. All returns are calculated after taking expenses, management and administration fees into account.

The FundGrade A+® rating is used with permission from Fundata Canada Inc., all rights reserved. Fundata is a leading provider of market and investment funds data to the Canadian financial services industry and business media. The Fund-Grade A+® rating identifies funds that have consistently demonstrated the best risk-adjusted returns throughout an entire calendar year. For more information on the rating system, please visit www.Fundata.com/ProductsServices/FundGrade.aspx.

FOR ADVISOR USE ONLY

The Empire Life Insurance Company 259 King Street East, Kingston Ontario 1 877 548-1881 info@empire.ca 8:30 am to 5:00 pm, EST weekdays

You are receiving this email as a valued distribution partner with Empire Life. For advisor use only.

®/™ Registered Trademark and Trademark of The Empire Life Insurance Company